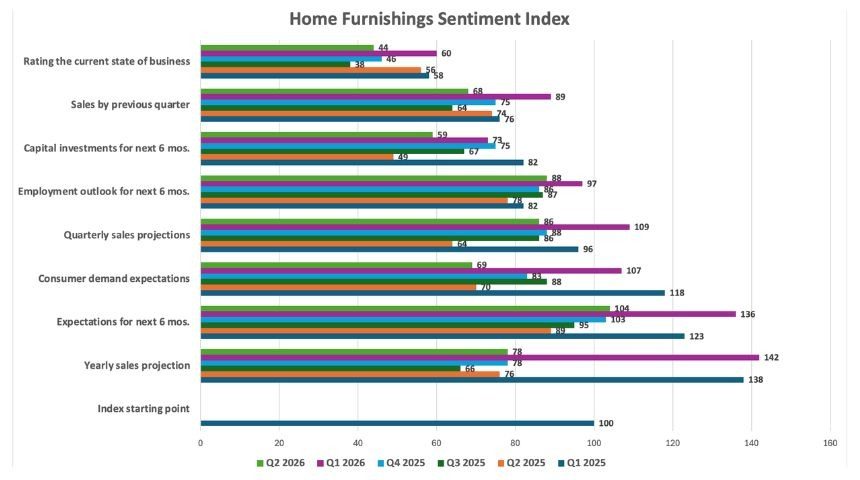

Q2 sentiment index shows positivity was short-lived

Joanne Friedrick //Research Editor//June 15, 2026

High Point, N.C. — It didn’t take long for the optimism bubble to burst for those responding to the latest Home Furnishings Sentiment Index survey, which tracks attitudes about current and future business within the industry.

Coming off an all-time high for above-average yearly sales projections with a score of 142, this quarter found participants expecting the year to end with sales on a downward trend, resulting in a score of 78, matching the fourth quarter 2025 outlook.

Expectations for the next six months of sales also dropped, although respondents were still somewhat more bullish on business in the short term with the metric reaching 104 on a scale where 100 is the starting point.

See also: Exclusive sentiment index reflects turnaround vibe

In line with the more somber approach in Q2, the current state of business rating found many more respondents characterizing it as fair or poor than good or excellent. In fact, no one rated business as excellent, and fewer characterized it as neutral. This resulted in a score of 44, the second lowest since the index was launched in Q1 2025.

Respondents also showed waning confidence in consumers returning to more typical home furnishings shopping behavior. The score for expected consumer demand fell by nearly 40 points since the first quarter to 69, marking its lowest to date.

Many concerns continue to plague the industry, with 82% of survey takers calling out the long-standing issue of sluggish housing and volatile mortgage rates as the No. 1 factor they are watching.

But more recent developments are rising on the list as well, including oil and gas prices, mentioned by 81%. With the war with Iran starting in late February, geopolitical conflicts vaulted in significance for 61%, up from 31% in the previous quarter.

Possibly linked to the war and oil and gas prices, supply chain issues gained ground as a factor as well, rising to a factor for 59%, up from 40%.

Tariffs, which were tied for the top factor in Q1, dropped to fourth at 71% as other issues emerged. Meanwhile, consumer sentiment appeared on more watch lists, up to 74% from 70%. About one-third or fewer cited labor and monetary policy and less than 20% were following AI adoption or immigration policy.

Index scores remained low on the topics of capital investments and hiring for the next six months, with both dropping in the second quarter. Employment, which reached an index high of 97 in Q1, fell to 88 in the second quarter as fewer respondents made plans to add staff. The capital investment score of 59 was the second lowest since tracking began.